What we do

We provide short-horizon predictive signals on limit order book designed to help algorithmic high-frequency traders build more advanced strategies, improve market making, execution timing, adverse-selection avoidance, and short-horizon alpha research. Our system delivers signals for limit order book features, including mid-price and micro-price movements, spread-crossing events and other short-horizon microstructure activity through a low-latency signal stream. The signals are typically refreshed 10 - 100 times per second depending on the asset, activity level and signal type. An individual signal looks like this:

| Timestamp | Asset | Task | Prediction | Confidence |

|---|---|---|---|---|

| 10:40:53.345167842 | ETH/USD | mid_price_direction | Up | 71% |

Why we do it

The dynamics of the limit order book are notoriously hard to model due to the noisy environment, irregular timing and cross-influence between market participants. Production trading systems typically rely on hand-engineered microstructure features and task-specific models, and while these can be effective, they often struggle to generalize across assets, regimes, and prediction tasks. ML models, on the other hand, handle the complexity better but require specialized architectures to keep up with the extreme speed of the markets. Very few trading companies have the depth of expertise required to develop them, and this is where we come in by offering the predictive power of ML models to traders at a latency suitable for the markets.

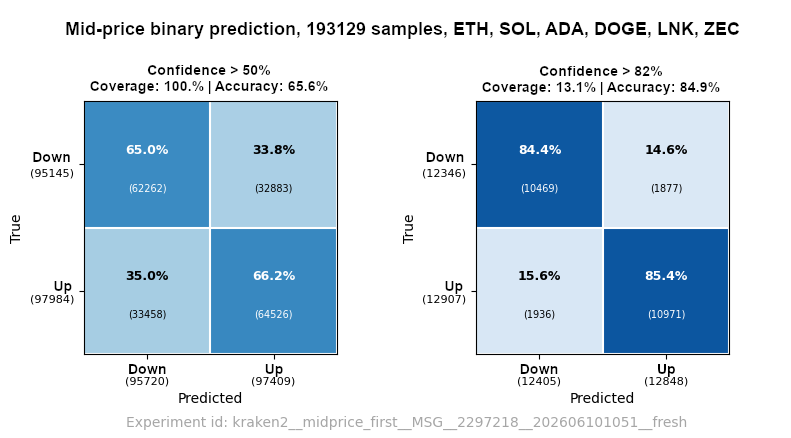

Results

Behind the scenes, the signals are produced by proprietary ML models built on over 10 years of research on state-of-the-art low-latency LOB modelling architectures in our group. Our latest model achieves 65% out-of-sample accuracy in predicting the direction of the next mid-price move, and 85% accuracy when acting on only the highest-confidence predictions (>10% of all predictions). The model's inference latency is <1 ms.

The above confusion matrix pair visualizes the prediction results of the model on 193k samples from 6 assets during 5 trading days without confidence thresholding (left) and with minimum threshold of 82% (right).

Interested?

We are now partnering with a small number of quant trading companies active on Kraken crypto exchange to pilot the signal stream. As a pilot partner, you get early access to the signals for your own trading or research workflow. In return, we are looking for practical feedback on latency, signal quality, use cases and deployment needs. Successful pilots continue into long-term access as we commercialize the technology during 2026. Reach out to anyone in our team below to ask about the pilot if you're interested.

About us

We are a research group at Tampere University with a decade-long history in leading research LOB modeling architectures such as TABL and LOBERT. Our core team:

- Prof. Juho Kanniainen - Investor and industry relations (juho.kanniainen [at] tuni.fi, Linkedin)

- Prof. Alexandros Iosifidis - Scientific research (alexandros.iosifidis [at] tuni.fi, Linkedin)

- Dr. Kestutis Baltakys - Core system development (kestutis.baltakys [at] tuni.fi, Linkedin)

- Mr. Eljas Linna - Product and go-to-market (eljas.linna [at] tuni.fi, Linkedin)